This article originally appeared in the Harvard Business Review

(with Richard Florida)

We’re used to thinking of high-tech innovation and startups as generated and clustered predominantly in fertile U.S. ecosystems, such as Silicon Valley, Seattle, and New York. But as with so many aspects of American economic ingenuity, high-tech startups have now truly gone global. The past decade or so has seen the dramatic growth of startup ecosystems around the world, from Shanghai and Beijing, to Mumbai and Bangalore, to London, Berlin, Stockholm, Toronto and Tel Aviv. A number of U.S. cities continue to dominate the global landscape, including the San Francisco Bay Area, New York, Boston, and Los Angeles, but the rest of the world is gaining ground rapidly.

That was the main takeaway from our recent report, Rise of the Global Startup City, which documents the global state of startups and venture capital. When we analyzed more than 100,000 venture deals across 300-plus global metro areas spanning 60 countries and covering the years 2005 to 2017, we discovered four transformative shifts in startups and venture capital: a Great Expansion (a large increase in the volume of venture deals and capital invested), Globalization (growth in startups and venture capital across the world, especially outside the U.S.), Urbanization (the concentration of startups and venture capital investment in cities — predominantly large, globally connected ones), and a Winner-Take-All Pattern (with the leading cities pulling away from the rest).

These major transformations pose significant implications for entrepreneurs, venture capitalists, workers, and managers, as well as policymakers for nations and cities across the globe.

The Great Expansion

The first shift is the Great Expansion, as the past decade has witnessed a massive increase in venture capital deployed globally.

The annual number of venture capital deals expanded from 8,500 in 2010 to 14,800 in 2017, for an increase of 73% in just seven years. The amount of capital invested in those deals surged from $52 billion in 2010 to $171 billion in 2017 — a gain of 231%. These figures represent historical records aside from the peak of the dotcom boom in 2000 (and may even exceed it). By all accounts, 2018 will be even bigger.

Globalization

The second shift is the accelerating Globalization of venture deals. For decades, the United States held a near monopoly on venture capital, where as late as the mid-1990s, the U.S. captured more than 95% of all venture capital investments globally.

That share has declined since then — gradually for the first two decades (falling to about three-quarters of the global total by 2012), and rapidly in the last five years (dropping to a little more than half by 2017).

Urbanization

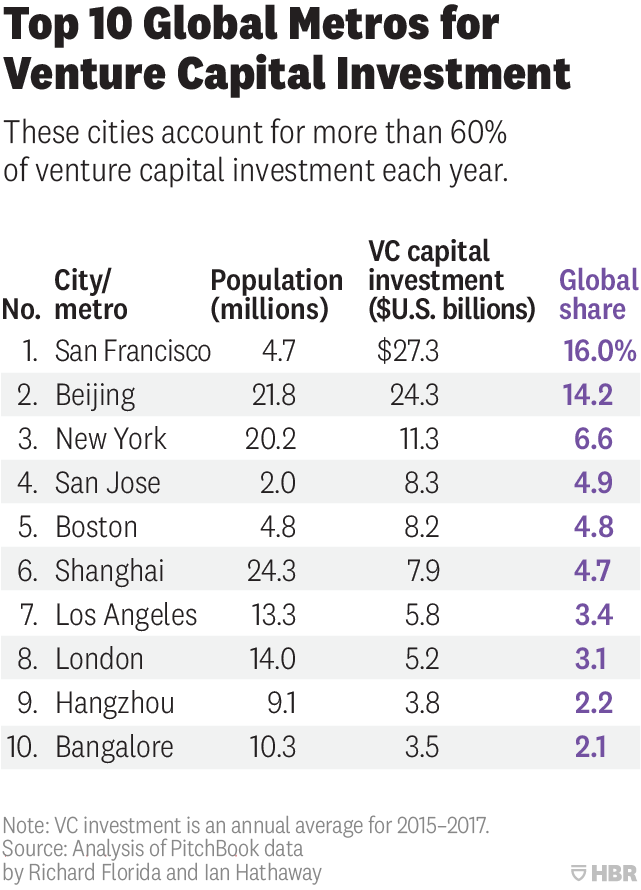

The third shift is the Great Urbanization of startup activity and venture capital activity in the largest global cities in the world. For decades, startups and venture capital activity was located in the quaint suburban office parks and low-rise office buildings of “nerdistans” like Silicon Valley, the Route 128 Beltway outside Boston, and the suburbs of Seattle, Austin, or the North Carolina Research Triangle. But our research shows that the startup activity and venture capital investment are now concentrated in some of the world’s largest mega-cities.

The table below shows the 10 leading cities for venture capital investment in the world. These 10 cities accounted for more than $100 billion in venture capital investment on average each year between 2015 and 2017, or more than 60% of the total. Three of the 10 leading global metros have populations in excess of 20 million people and three more have populations of between 10 and 15 million. Three more cities have between 4 and 10 million people, while one has less than 2 million (San Jose, the heart of Silicon Valley).

A separate study by one of us and a colleague that looked at the factors associated with venture capital investment across U.S. metros found population size and density to be key. The only other factor that was slightly more important was high-tech industry concentration, which is what entrepreneurs and venture capitalists are aiming to create over the long run.

Winner-Take-All Geography

Startups and venture capital increasingly take on a winner-take-all pattern geographically. Venture capital investments are highly concentrated geographically. Just the top five cities account for nearly half of the global total, and the top 25 for more than three quarters of global venture capital investment. And, previous research one of us has done for the United States and globally, shows that even within cities, venture capital activity tends to be highly concentrated among just a few postal codes.

The geographic concentration of venture capital has also increased over the last decade. This is particularly the case at the very top, where the top 10 cities account for 61% of venture activity worldwide in the latest three-year period, but just 56% a decade ago. Given the large amount of underlying activity going on each year, even small percentage point changes represent meaningful shifts in concentration.

Forces Behind the Shifts

We can point to three major factors driving these trends, though there are others. The first is technological, as the confluence of high-speed internet, mobile devices, and cloud computing has made it possible to start and scale digitally-enabled businesses at a fraction of the cost. As these technologies have fallen in cost, they are within reach in more markets, meaning that it’s easier to create and grow these high-growth, high-tech businesses in more cities.

The second factor is economic. The world has just gone through the largest global reduction in poverty and concomitant expansion of the global middle class in history, and multi-national corporate giants are emanating from more countries, particularly in emerging markets. This has increased demand for many digital goods and services in more places, giving technologically-enabled entrepreneurs in more places a robust market to sell into.

The third factor is political. Many nations around the world are doing more than ever to compete on a global stage by improving their education systems and universities, investing more in research and development, and bending over backwards to welcome high-skilled foreigners and company founders. The United States, on the other hand, is sliding backwards on all of these fronts — and in our view, has become complacent with its long-held dominance as a monopoly for high-tech entrepreneurship.

What It Means for Leaders

These trends have important implications for entrepreneurs, investors, managers, and workers, as well as national and local policymakers across the world. For entrepreneurs, it’s fairly straightforward. The San Francisco Bay Area remains by far the leading location for venture activity and the most robust ecosystem for growing a high-tech startup by a long shot. However, many of the key resources found in The Valley are increasingly available in other places. Whether non-American founders can’t obtain a U.S. visa or choose to stay at home for other reasons, it will only get easier for them to do so while building their companies.

For investors and corporations, the big takeaway is this: You can no longer look only in your own backyard for startups, innovation, and the talent that power them. Venture capitalists, used to looking close to home, need to broaden their horizons and think, look, and act globally. Corporate managers, especially those in the United States, are used to strong local sources of innovation, but they too must increase their awareness of global innovation and startups as they look to as address competitive threats and capture new sources of innovation. Large established corporates may see opportunities in building globally disturbed teams. Techies and entrepreneurs around the world can count on greater opportunities in their home markets.

For global policymakers, the lesson is that globalization of high-tech entrepreneurship and venture capital mean greater competition across the board. For U.S. policymakers, they can no longer take its long-established lead in innovation and startups for granted. China is nipping at its heels and other nations are also gaining ground quickly. Sure, the US remains the dominant place by far, but it is time to stop doing counterproductive things like imposing immigration restrictions on highly-skilled individuals and founders with validated business ideas. Such actions chill the climate for global talent. For countries that are emerging on the global stage, it means continuing and even expanding on recent improvements in education, innovation, and immigration. For the world as a whole, having entrepreneurs and techies build companies where they are may eventually help to address the growing spatial inequality and winner-take-all dynamics that currently define the global geography high-tech startups.

Of course, innovation and entrepreneurship are local, not national, games. That means mayors and city leaders must take the lead. And it means nations should consider devolving responsibility for innovation and economic policy functions to the local level, especially as most countries will only have one or a few cities that can compete on a global stage. But it does not mean throwing government money at venture capital, which too many national and local governments tend to do. Instead it means investing in local universities and innovation, creating greater local density, and generating the kind of quality of local talent. And it also means working with the private sector not just to improve the preconditions required for innovation and startups, but to address the growing economic inequality and housing unaffordability that is causing a growing backlash against big tech in cities across the globe.